How Digital Assets Are Reshaping Cross-Border Finance

June 4, 2026

Positioning line: “Digital assets are reshaping finance. UAB Exchange helps you stay informed, prepared, and connected to the market.” Target keyword: crypto cross-border payments. Secondary keywords: digital assets remittance, stablecoin payments. Search intent: Informational. Funnel stage: TOFU — thought leadership. Meta description (155 ch): Stablecoin settlement now moves more value across borders than some major remittance corridors. Why digital assets are quietly rewriting global finance. CTA: Read UAB Exchange’s quarterly market intelligence.

Most of the public conversation about digital assets is about prices. The more consequential story — the one that will define the next decade of global finance — is about settlement.

Traditional cross-border payments run on infrastructure that is sixty years old. A wire from a bank in London to a bank in Karachi typically touches four to six intermediaries, takes one to three business days, costs the sender between three and seven percent depending on amount, and arrives with foreign exchange margins that are rarely disclosed transparently. This is not because the technology is incapable. It’s because the rails are built around a settlement model designed for an era of telex machines and physical correspondent banking.

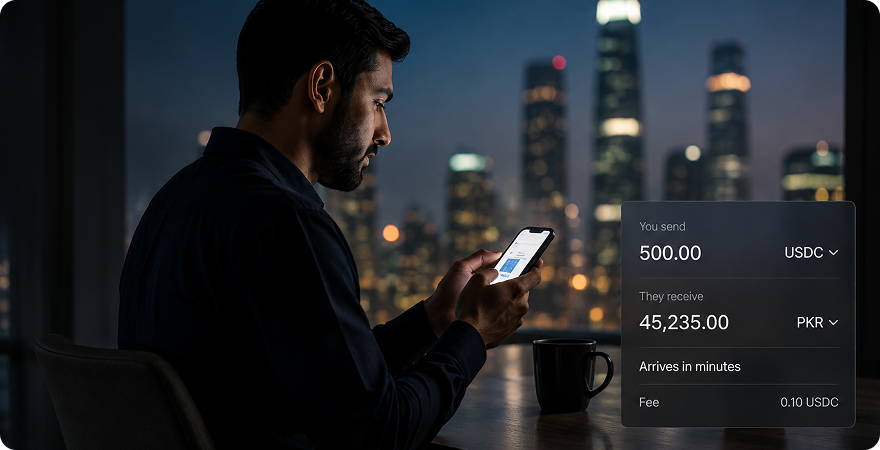

Stablecoins changed the underlying economics. A USDT or USDC transfer settles in minutes, costs cents in network fees regardless of size, and clears without intermediaries. The implication is not theoretical: stablecoin annual settlement volume now exceeds the total throughput of several major card networks, and in 2024 it began routinely exceeding Visa’s settlement volume on certain measurement windows. A meaningful share of that flow is genuine cross-border payments rather than crypto-native trading.

Where the impact is showing up first.

Three corridors are leading. Emerging-market remittance: workers in the Gulf and in Europe sending money to South Asia and Africa are increasingly settling in stablecoins on one end and converting at the destination, bypassing the traditional remittance rails entirely. B2B trade settlement: small and mid-size importers and exporters use stablecoin payment to avoid the friction of correspondent banking and to settle outside the working hours of traditional rails. Treasury operations: corporate treasurers in countries with capital controls or currency volatility use stablecoins as a digital dollar substitute when local options are constrained.

What this does not mean.

It does not mean banks are being replaced. The settlement layer is changing, but the customer relationship, regulatory compliance, fraud monitoring, and last-mile fiat conversion still sit with regulated financial institutions. The pattern emerging is closer to “stablecoins as plumbing” — invisible to most end users, but doing the actual work behind familiar interfaces.

The regulatory direction is clarifying, not tightening.

The EU’s MiCA framework, the UK’s stablecoin regime, Singapore’s payment services framework, and the US stablecoin legislation moving through Congress are different in detail but converging on a consistent shape: licensed issuers, full reserve backing, mandatory disclosures, and clear consumer protections. This is the opposite of the uncertainty that defined the previous cycle. For businesses considering integration, the regulatory path is now more visible than it has been at any point in the asset class’s history.

What this means for someone watching the space.

Two things. First, the most interesting use cases for digital assets are no longer speculative; they’re operational. Payment, settlement, treasury, and FX management are where the substantive integration is happening. Second, the line between “crypto company” and “financial company” is getting blurry — and the institutions that adapt early to the convergence will define the next phase of the industry.

UAB Exchange operates at this intersection. The digital-asset market is no longer a parallel financial system. It’s becoming part of the main one.